Best Mutual Funds for SWP in India: How to Choose the Right Fund for Regular Income

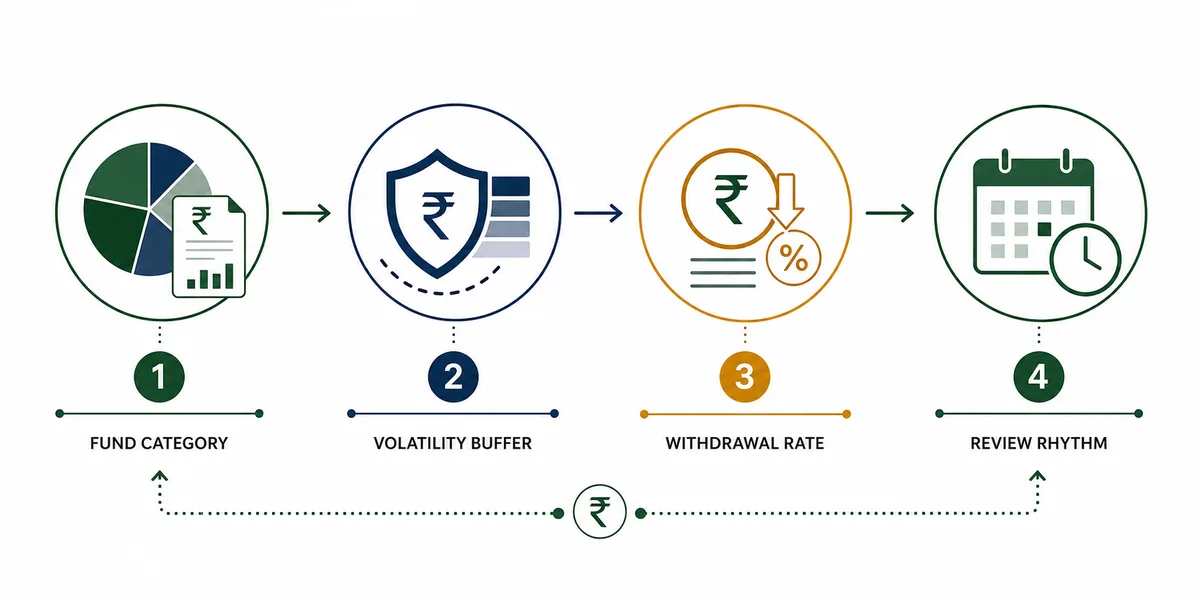

The best mutual fund for SWP is not simply the fund with the highest past return. It is the fund category, risk level, withdrawal rate, and review process that can support regular income without taking more market risk than your corpus can handle.

Quick answer

For most Indian SWP investors, the shortlist should start with a conservative hybrid, balanced advantage, equity savings, short duration debt, or a well-diversified equity fund depending on the time horizon. Then test the planned monthly withdrawal in a SWP calculator, compare inflation impact, and reject any fund where the withdrawal rate only works under optimistic returns.

Table of Contents

How to Define the Best SWP Fund

A Systematic Withdrawal Plan is a facility for withdrawing a fixed amount from an existing mutual fund investment at regular intervals. That means the fund you choose has to do two jobs at once: support regular redemptions and keep enough corpus invested for future years. A fund that looks attractive during accumulation may be too volatile when you start withdrawing every month.

The better question is not “which SWP fund gives the highest return?” but “which fund can support my required income with acceptable volatility, tax impact, and review discipline?” For a retiree who needs monthly expenses, a smoother fund may be more useful than a fund with a higher long-term return but deep drawdowns. For an early-retirement investor with a 20-year income horizon, some equity exposure may still be needed to fight inflation.

| Selection factor | What to check | Why it matters for SWP |

|---|---|---|

| Time horizon | How many years the income must last | Longer horizons usually need growth assets, while short horizons need more stability. |

| Withdrawal rate | Annual withdrawal divided by starting corpus | A high withdrawal rate can deplete the fund even when average returns look good. |

| Volatility | Fund category, riskometer, drawdowns, and portfolio mix | Market falls early in SWP can force more units to be sold at lower NAVs. |

| Liquidity and exit load | Scheme rules, lock-in, exit load period, redemption timelines | Regular withdrawals need operational flexibility. |

| Tax treatment | Equity or debt taxation, holding period, capital gains | The net income after tax can differ from the calculator's gross withdrawal. |

Best Fund Categories for SWP: Practical Comparison

No category is automatically best. The fit depends on the investor's income dependency and ability to tolerate corpus fluctuation. Use the table below as a first filter, then compare actual schemes inside the chosen category.

| Fund category | SWP fit | Better for | Main caution |

|---|---|---|---|

| Balanced Advantage / Dynamic Asset Allocation | Often useful for medium to long SWP plans | Investors who want equity participation with managed allocation | Allocation model and category behavior can differ widely by AMC. |

| Conservative Hybrid | Useful for lower-volatility income planning | Retirees who need steadier corpus movement than equity-heavy funds | Returns may not fully offset high inflation or aggressive withdrawals. |

| Equity Savings | Can suit moderate-risk SWP investors | Investors wanting a mix of equity, arbitrage, and debt exposure | Strategy complexity makes scheme-level review important. |

| Short Duration / Corporate Bond Debt Funds | Useful for near-term withdrawal buckets | Investors prioritizing lower volatility and liquidity | Credit risk, interest-rate risk, and tax treatment still matter. |

| Large Cap / Flexi Cap Equity Funds | Possible for long SWP horizons with a buffer | Investors with other income sources or flexible withdrawals | Sequence-of-returns risk can be high during market declines. |

If the SWP will pay essential household expenses, avoid building the whole plan around a single aggressive equity fund. A bucket approach can be more practical: keep 1-3 years of planned withdrawals in lower-volatility funds, keep the medium-term bucket in hybrid/debt categories, and keep long-term growth exposure only for money that can tolerate fluctuation.

Check the Withdrawal Rate Before Looking at Fund Names

Many investors search for the best SWP mutual fund after already deciding a monthly withdrawal. That order is risky. First calculate whether the withdrawal itself is reasonable. For example, ₹40,000 per month from a ₹50 lakh corpus means ₹4.8 lakh per year, or a 9.6% starting withdrawal rate before taxes. That is aggressive for many retirement portfolios, especially if withdrawals rise with inflation.

Start with a few stress cases:

- Base case: expected return based on the fund category, current monthly withdrawal, and selected period.

- Low-return case: reduce the assumed return by 2-3 percentage points to see whether the plan still survives.

- Inflation case: use the SWP calculator with inflation to see real purchasing power.

- Step-up case: use the SWP calculator with annual increase when expenses are expected to rise each year.

Conservative planning note

This page is educational and does not recommend a specific scheme. Mutual fund returns are market-linked, and SWP withdrawals sell units at future NAVs that cannot be known today. Before placing an instruction, read the scheme documents and consider advice from a qualified financial adviser.

Risk Checks Before Selecting an SWP Fund

SWP planning has a different risk profile from SIP accumulation. In SIP, market dips can help you accumulate more units. In SWP, a market dip can force you to redeem more units for the same cash amount. This is why volatility and early-year returns matter.

Check the riskometer and portfolio

SEBI's mutual fund riskometer framework is designed to label scheme risk. Use it as a starting point, then read the portfolio, asset allocation, credit quality, and maturity profile rather than relying only on the category name.

Avoid return-only selection

The highest one-year return can come from a fund that took more risk. For SWP, consistency, downside control, expense ratio, tax fit, and suitability are often more important than last year's rank.

Review after market shocks

If the corpus falls sharply, do not blindly continue the same withdrawal. Recalculate with current corpus, lower return assumptions, and a temporary reduction in withdrawal if needed.

Separate needs from wants

Essential expenses should usually be funded from a more stable bucket. Flexible lifestyle expenses can be linked to higher-growth funds because they can be reduced in weak markets.

Example: Building a Shortlist for a ₹60 Lakh SWP Corpus

Assume an investor wants ₹30,000 per month from a ₹60 lakh mutual fund corpus. The first-year withdrawal is ₹3.6 lakh, or 6% of the starting corpus. That is not automatically unsafe, but it needs careful testing because inflation, tax, and market volatility can push the effective burden higher.

- Run the base calculation. Use a 7-9% return range in the main SWP calculator rather than assuming a high equity return.

- Test inflation. If the withdrawal needs to rise every year, compare 4%, 6%, and 8% inflation cases.

- Choose candidate categories. For this profile, balanced advantage, conservative hybrid, equity savings, or a debt-plus-hybrid bucket may be more relevant than a single aggressive equity fund.

- Reject operational mismatches. Avoid funds with unsuitable exit load windows, scheme restrictions, or risk levels that do not fit the investor's comfort.

- Review annually. Recalculate using the current corpus, current withdrawal, and updated assumptions at least once a year.

If the same investor still has 10 years before starting withdrawals, the decision changes. They may use a SIP SWP calculator to estimate how much corpus can be built first, then choose a more balanced withdrawal portfolio closer to retirement.

Where This Page Fits With Existing SWP Tools

Use this guide to decide what kind of fund category belongs in your shortlist. Then use the calculator pages to test numbers:

Corpus durability

Estimate withdrawals, remaining balance, and charted corpus movement.

Open SWP CalculatorPlatform comparisons

Compare calculator features from platforms and fund houses.

Compare calculatorsOfficial References Worth Checking

Before choosing a real scheme, use official and primary resources to understand withdrawal rules, scheme risk, and investor information:

- Mutual Funds Sahi Hai SWP calculator for investor-awareness context around SWP projections.

- SEBI circular on mutual fund risk-o-meter for scheme risk labeling.

- AMFI Investor Corner for investor resources, disclosures, and mutual fund awareness material.

- Mirae Asset explanation of SWP for a fund-house description of systematic withdrawals.

FAQ

Bottom Line

The best SWP mutual fund is the one that fits the withdrawal plan after stress testing, not the one with the loudest return number. Shortlist fund categories first, test the withdrawal rate, check risk and liquidity, then use calculator outputs as a planning estimate rather than a promise.